来自中国电池电芯制造商的成本压力、欧盟在电池电芯领域更侧重可持续发展而非价格优势、缺乏成熟的磷酸铁锂(LFP)电芯制造生态系统,以及政策框架不够明确,这些都是削弱欧盟挑战大中华区在电池领域主导地位能力的核心威胁。

近期,欧洲和英国地区接连有几家备受瞩目的电池公司突然申请破产,给该地区发展本土电池生产的雄心造成了重大打击。

英国颇具前景的电池初创企业Britishvolt曾受到该国首相的盛赞,但于2023年1月申请破产。 紧随其后的是瑞典电池公司Northvolt,该公司曾代表欧洲对抗中国在全球电池供应链中主导地位的希望。2024年11月,该公司在美国申请了第11章破产保护。

尽管当时Northvolt管理层曾预期能够获得新资金——包括1.45亿美元的现金抵押以及斯堪尼亚(Scania)承诺的1亿美元——以维持其瑞典主工厂的运营,但这些计划最终未能实现。 该公司最终于3月在瑞典申请破产。鉴于Northvolt在维持流动性方面举步维艰,且其困境对沃尔沃与Northvolt合资企业Novo Energy的未来造成影响,这家瑞典汽车制造商于1月采取行动,全资收购了该电池合资企业。与此同时,据路透社5月22日报道,Northvolt预计将在6月底前逐步停止其位于谢莱夫特奥工厂的剩余电池电芯生产业务。

德国电池制造商CustomCells(弗劳恩霍夫协会的分拆公司)于4月30日申请破产,此前其最大客户、航空航天公司Lilium已宣告破产。

大约在去年同一时期,梅赛德斯-奔驰、Stellantis和法国能源公司道达尔能源(TotalEnergies)共同成立的备受瞩目的电池合资企业Automotive Cells Company(ACC),暂停了其计划在德国和意大利各建一座超级工厂的建设,旨在重新评估其电池化学成分战略。 据悉,ACC的母公司正在评估比高镍NCM(镍钴锰)电池更具成本优势的替代方案,而该公司在法国超级工厂生产高镍NCM电池已有一年时间。

受现金流紧张及电动汽车需求放缓的困扰,挪威电池制造商FREYR Battery于2024年缩减了业务规模,放弃了扩张计划,并暂停了位于莫伊拉纳的“北极超级工厂”(Giga Arctic)的电芯生产。今年早些时候,该公司将名称从FREYR更名为T1 Energy,将总部从挪威迁至得克萨斯州奥斯汀,以最大限度地享受美国税收优惠,并将业务重心转向太阳能应用领域。

欧盟的电池制造生态系统为何迟迟未能起飞?

PowerCo首席执行官弗兰克·布洛姆(Frank Blome)在最近接受Battery Associates采访时坦率地指出,在电动汽车发展的早期(21世纪初),当西方国家尚未看到电动出行领域的商业价值时,日本、韩国和中国已经开始大规模生产用于笔记本电脑、手机、混合动力汽车和电动汽车的电池。

“通过这样做,他们实现了规模化生产并不断改进生产工艺,”他表示。

相比之下,欧盟委员会直到2017年才意识到欧盟亟需建立本土电池产业链,并由此启动了“欧洲电池联盟”(EBA)。随后在2018年,欧盟推出了首份电池领域的“欧盟战略行动计划”。这表明,与大陆中国及其他东方国家相比,欧盟在发展本土电动车电池产业链方面仍处于初期阶段。

布洛姆将电池生产业务称为“成本密集型”,他表示,在PowerCo高管每周的例会上,80%的时间都用于讨论成本问题。

此外,他还特别强调了中国大陆政府为设立电池制造企业的公司提供的多层次支持体系,包括直接和间接的资金支持、快速投产和项目审批,从而加速工厂建设;以及能源补贴、退税、免费使用特定经济开发区建造的厂房等激励措施,此外还有多项其他优惠。

“欧洲或德国没有任何一个体系能像这样运作。但我们必须尽快在这里做得更好,”布洛姆表示。

虽然布洛姆概述了欧洲在建立具有竞争力的电动车电池价值链方面面临的若干关键挑战,但深入探究欧洲在电池领域与大陆中国竞争中持续受挫的根本原因至关重要。

a) 成本压力与纯电动车(BEV)市场接受度低迷

一方面,中国电池电芯制造商在规模和成本上占据全球电池生态系统的顶端,其激烈的竞争持续施压;另一方面,纯电动车(BEV)的市场接受度低于预期,这两者共同构成了当地电池企业在欧盟地区建设超级工厂面临的最大挑战。

纯电动汽车(BEV)的普及滞后不仅会对新建超级工厂的投资产生负面影响,导致投资者采取谨慎态度,还将对现有电池企业的运营可行性造成巨大压力。电池需求不足已对CustomCells、FREYR Battery和ACC造成严重打击,这些企业因纯电动汽车普及速度低于预期以及成本压力,已决定暂停其在德国和意大利即将建成的超级工厂的建设。

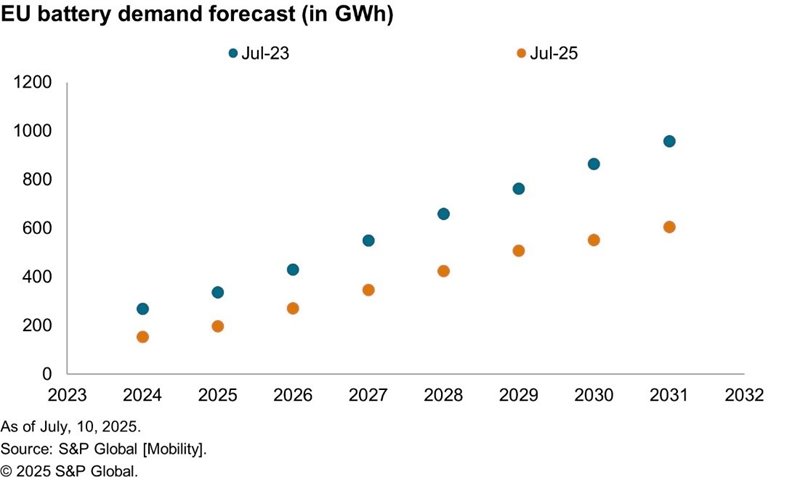

下图展示了标普全球移动(S&P Global Mobility)对2024年至2031年欧盟电池需求的修订预测。可以看出,由于纯电动汽车(BEV)的普及速度低于预期,欧盟地区对电动汽车电池的需求预测已被下调。就2025年而言,欧盟电池需求的修订值较此前预期下降了40%以上。 同样,2030年的修订后需求量较此前预测的规模下降了36%以上。

暂且不论纯电动汽车(BEV)的普及速度缓慢,若分析导致成本压力的根源,我们会发现若干人口结构和地缘政治因素,这些因素在维持现状的情况下,对发达的西方国家而言既难以应对又错综复杂。例如,欧盟新兴的电池制造生态系统仍处于初级阶段,其生产流程与大陆中国不同,既新颖又未经过优化。 欧盟不仅面临着比中国大陆高出许多的劳动力和能源成本,还需承担将关键电池材料从数千英里外的原产地运输至欧盟的费用。

相比之下,如果我们观察中国大陆的顶级电池企业,如宁德时代(CATL)和比亚迪(BYD),会发现它们不仅享受了免税政策和针对研发(R&D)活动的专项资金支持,还获得了包括直接补贴在内的多种政府支持。

媒体报道显示,2018年至2022年间,比亚迪获得了约37亿美元的直接补贴。同样,宁德时代的年报显示,该电池制造商获得的政府补贴从2018年的7670万美元增至2023年的8.092亿美元。 中国大陆另一家领先的电池制造商EVE Energy仅在2023年就获得了约2.089亿美元的政府补贴。

要了解中国大陆(尤其是省级层面)的政府支持,关键在于评估 中国西北部甘肃省的地方政府是如何协助这家名气较小的电池制造商——甘肃金鸿祥新能源有限公司,在短短半年左右的时间内,从零开始实现日产25万块电池的。

甘肃省政府为超级工厂项目提供“全生命周期服务”,涵盖从快速投产到项目进展及交付的全程监管。金昌经济开发区——金鸿祥新能源工厂所在地——免费向该公司提供了“拎包即用”的标准化厂房,为企业节省了生产成本和时间。 此外,当地政府还组建了专门的项目管理团队,成员涵盖发展改革、环保及安全监管等各部门代表,仅用30天就完成了15项政府审批手续。

除上述支持措施外,地方政府还提供设备折旧补贴等激励政策。

政府此类优惠政策确保企业能够专注于产品研发,同时甘肃省还拥有丰富的关键原材料本地供应,这进一步降低了物流成本。文章指出,与大中华区沿海地区的工厂相比,这些因素使甘肃省每块电池的制造成本降低了约12%。

电池制造中优化流程如何带来显著改善,其相关例证可从超级工厂的废品率中体现。该指标反映了制造过程中被浪费的材料数量——尤其是锂、镍和钴等高成本原材料。因此,较高的废品率会导致生产成本上升,并降低物料处理效率。

中国大陆的现有厂商已实现非常高效的工艺,废品率低于10%。然而,全球其他地区的电池初创企业由于缺乏专业技术,在产能爬坡阶段面临严重的质量问题,导致废品率高达30%-40%。北伏(Northvolt)在尝试扩大其位于舍莱夫特奥(Skellefteå)的电池工厂产能时,就曾因高废品率而备受困扰。

标普全球移动(S&P Global Mobility)电池研究经理阿里·阿迪姆(Ali Adim)指出,对于现金流本已为负的电池初创企业而言,解决废品率问题关乎生存存亡。

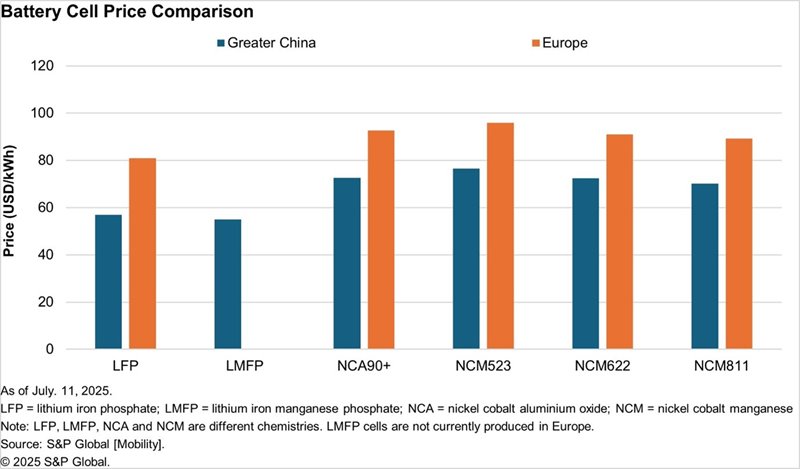

下图基于标普全球移动的电池电芯价格数据,对比了大中华区与欧洲生产的常见化学体系电芯价格。 该图表不仅凸显了磷酸铁锂(LFP)电芯相较于在欧美更广泛使用的镍钴锰(NCM)组合电芯在价格上的优势,同时也强调了即便西方电池厂正纷纷采用LFP电芯技术,中国大陆仍占据着主导地位。中国电池制造商之所以能取得这一成就,主要得益于其运转顺畅的供应链、成熟且优化的生产工艺以及政府的支持。

此外,必须指出的是,尽管LFP电池的成本低于每千瓦时60美元,但在大中华区,LMFP电池的价格更为实惠,约为每千瓦时55美元。这不仅使LMFP电池成为值得关注的关键电池化学体系,而且目前该电池仅在大中华区生产,欧盟尚未生产,这为北京提供了又一个巨大的优势。

值得注意的是,与LFP电池相比,LMFP电池在正极中添加了锰元素,从而实现了更高的能量密度。然而,在系统层面将LMFP技术整合到大规模生产中仍面临挑战。

与此同时,Blome在最近的采访中承认了优化生产流程在电池制造中的优势,并表示PowerCo目前正在学习标准生产流程。在萨尔茨吉特工厂今年投产后,该公司将在西班牙建设第二座更现代化、更优化的超级工厂,随后在加拿大建设第三座超级工厂。

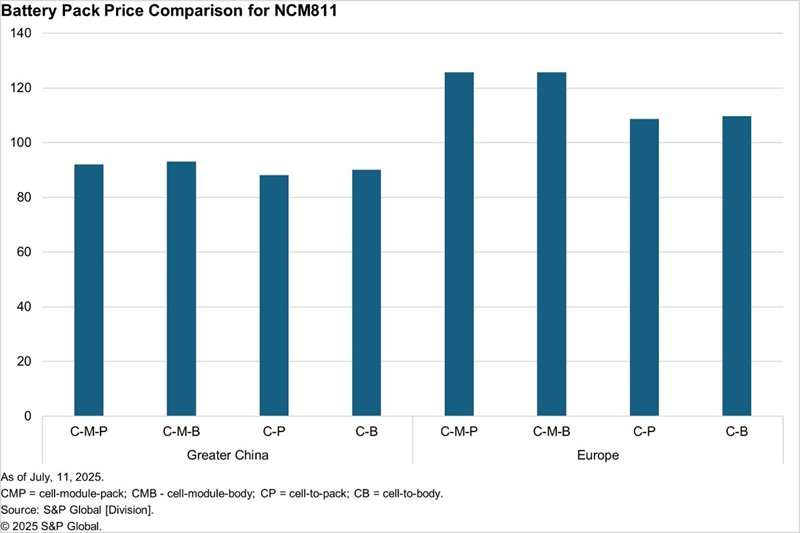

根据标普全球移动(S&P Global Mobility)的电池价格数据,在大中华区,NCM811电池组的总价格(包括电芯、模组及电池包价格)约为每千瓦时92美元,而欧洲则约为每千瓦时126美元。 下图展示了电池制造商提供的多种组合方案(如电芯-模组-电池包(CMP)、电芯-模组-车身(CMB)、电芯直装电池包(CP)和电芯直装车身(CB))下,NCM811电池包价格的差异。

对于采用“电芯到电池包”配置的磷酸铁锂(LFP)电池包,标普全球汽车(S&P Global Mobility)的数据表明,大中华区的电池总价格约为每千瓦时75美元,而欧洲则约为每千瓦时102美元。此处比较的价格针对的是“电芯到电池包”配置下的棱柱形磷酸铁锂电池。

b) 欧盟押注可持续性而非经济性

Northvolt作为全球资金最雄厚的电池初创企业之一,却在早期便遭遇了财务危机,这正是理解欧洲过度关注可持续性的绝佳案例。Northvolt的联合创始人兼首席执行官彼得·卡尔森(Peter Carlsson)曾任特斯拉供应链负责人,他选择在瑞典建立超级工厂,旨在利用该地区丰富且廉价的清洁能源,将碳足迹降至最低。

在斯凯莱夫特奥(Skellefteå)建设电池电芯超级工厂Northvolt Ett的同时,公司管理层还致力于整合上游业务,旨在建立一个闭环循环系统。该系统不仅能确保电池原材料来源的透明度,还计划到2030年实现高达50%的电池生产原材料来自回收利用。 为实现这一目标,这家资金雄厚的企业投资在Northvolt Ett旁建设了一座功能齐全的回收设施——Revolt Ett。

这家电池初创公司还投资在舍莱夫特奥建立了Upstream 1 CAM生产设施。但其布局远不止于此。 该公司还投资建设了硫酸钠回收基础设施——这种盐是生产阴极活性材料(CAM)时的副产品。值得注意的是,每生产一公吨CAM,最多可产生两公吨硫酸钠。Northvolt坦言,跨行业的标准做法是依法将这种硫酸钠作为废料排入河流和海洋。 但该公司却不遗余力地打破这一惯例,投入资源对这种盐类副产品进行净化处理,将其升级再造为商业产品。建设此类基础设施耗资巨大,只有当Northvolt实现大规模运营时才能获得回报。然而,该公司未能如期将核心业务扩展到电池电芯生产,未能兑现对客户的承诺。

Northvolt Ett工厂第一阶段本应具备16GWh的年产能,但2023年仅安装了1GWh产能。尽管如此,这1GWh产能的利用率几乎为零,因为该公司除微不足道的试产量外,几乎未生产任何电池电芯。在电芯交付延迟两年后,宝马于2024年取消了价值20亿欧元的电池电芯订单。

毫无疑问,该公司曾坚定致力于生产“绿色”电芯,但其发展重心过早分散,尤其是在本应专注于完成价值500亿美元订单以实现规模化生产的关键时期。若当初避免在回收及其他周边业务上投入资金,本可节省宝贵的现金流,进而用于解决导致斯凯莱夫特奥电芯生产延误的问题,从而确保企业生存。

欧洲对可持续发展的承诺以及《绿色协议》中概述的雄心勃勃的目标——包括到2050年实现气候中和以及将交通排放减少90%——正给那些依赖资本密集型硬件的新兴清洁技术企业带来巨大压力。这种情况形成了一个两难困境,因为欧盟的最佳选择是生产碳足迹低于中国大陆制造的“绿色”电池。

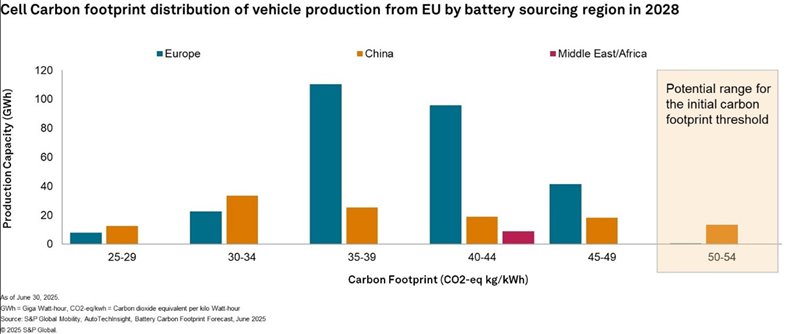

此外,欧洲电池初创企业生态系统一直押注于原始设备制造商(OEM)会因其对可持续性的重视而为其产品支付溢价。然而,阿里指出,事实证明,中国电池制造商并非只是旁观欧盟地区的同行,而是通过对其电池价值链的多个环节进行脱碳,提供了比欧洲企业更低的碳足迹。

下图展示了大中华区与欧洲生产的电池电芯碳足迹对比。尽管产能庞大,但得益于对碳排放的有效管控,大中华区电池电芯生产的平均碳足迹低于欧洲。

c) Lack of an Established LFP Manufacturing Ecosystem in Europe

While the choice of battery chemistry significantly influences the cost structure of a BEV or a plug-in hybrid electric vehicle (PHEV), it is known that the lithium iron phosphate (LFP) batteries offer a cost advantage as compared to the more widely used lithium nickel cobalt manganese oxide (NMC) batteries. Notably, the LFP batteries are understood to be about 30% less expensive per kilowatt-hour compared to the NMC batteries, which continue to be the predominant chemistry used by the automakers in the US and Europe.

In contrast, the LFP batteries are more widely used in mainland China, the world’s largest EV market, giving the Chinese battery makers a significant advantage on the cost parameter. This also stemmed from the licensing agreements that the Chinese battery makers had with the patent holders — mainly universities in the US and Canada — over the years. This helped the Chinese companies in integrating the technology in their manufacturing processes while continuing to enhance it in their respective R&D labs.

Meanwhile, Korean and Japanese battery makers focused more on high-density, nickel-rich battery chemistries such as NCM and NCA, giving very limited attention to the applicability of affordable LFP battery cells.

That said, key patents of LFP battery technology began expiring by 2022, giving wider access to global battery companies. This shift coincided with global automakers’ ongoing pursuit to reduce the development and manufacturing cost of EVs to achieve wider adoption.

In 2020, Tesla adopted LFP batteries, moving away from NCA cells. The move was aimed at avoiding nickel, a supply chain-constrained metal, and cobalt, which came from the infamous mines of the Democratic Republic of Congo. Tesla’s battery competency and cost structures sparked interest among rivals such as Ford Motor Company, General Motors and Volkswagen, who followed suit.

Although NMC batteries continue to provide higher energy density when compared to the LFP cells, the gap has narrowed in recent years, thanks to the significant technology advancements made by Chinese battery makers.

Reports suggest that the energy density of LFP battery packs is about one-fifth lower by mass (Wh/kg) and about one-third lower by volume (Wh/L) than that of NMC packs. This performance deficit, however, is compensated by a superior thermal stability, safety and a longer life cycle as compared to the NMC battery packs.

That said, the EU has an upcoming LFP battery cell manufacturing ecosystem. According to official announcements, it is expected that CATL will likely lead the efforts to localize the production of LFP battery cells in the region. The company, which already has two plants operational in the EU region, signed two key strategic partnerships in 2024. It signed a deal with Renault to provide the French carmaker with LFP battery cells from its Hungary plant, as well as entered into an equal joint venture with Stellantis to set up LFP battery cell gigafactory in Spain.

In addition, LG Energy, which produces NCM battery cells at its Poland-based facility, plans to add LFP cells at Renault's site.

VW’s PowerCo, which has fast charging LFP cells on its test benches at Salzgitter, is on track to commence production at the site later this year.

d) Too Many, Indistinct Policy Interventions

The European Commission launched its first-ever dedicated ‘strategic action plan’ for batteries in 2018. The action plan was aimed at securing access to battery-critical raw materials, especially the materials that are not available in Europe, from resource-rich countries, supporting battery R&D, promoting sustainable battery cell manufacturing and recycling, developing a highly skilled workforce to contribute to the battery value chain, among other areas. The action plan included a funding of €360 million to promote battery R&D and €270 million to similar projects dedicated to smart grid and battery storage under Horizon 2020. That said, there was no explicitly mentioned funding available for companies putting factories to produce batteries in the EU region at that time. For context, SK On had just begun the construction of its battery plant in Hungary in early 2018, and LG Energy Solution had already established its first battery plant in Europe in Poland in 2016.

Over the years, the European Commission has rolled out several regulations aimed at promoting the local battery ecosystem, such as the Critical Raw Materials Act, Circular Economy Action Plan, Net Zero Industry Act, New Batteries Regulation 2023, which included the battery passport mandate, and the latest Industrial Action Plan for the automotive sector, which was released in March.

To boost battery manufacturing in Europe, the latest industrial action plan launched a “battery boost” package, which makes funding of €1.8 billion available over 2025-27 to support companies manufacturing batteries in the EU. This is in addition to the €3 billion that the commission has already announced earlier.

However, policymakers are still exploring the possibility of providing direct production support to companies producing batteries in the EU. The commission is also exploring if specific state aid can be provided to such companies and is working to prepare a new Clean Industrial State Aid Framework to simplify state aid rules. In addition, policymakers are also exploring the possibility of introducing specific European content requirements on battery cells and components in EVs sold in the EU region. The paper also mentioned that the commission is assessing whether interventions on standardizing battery designs could be beneficial for battery startups in the critical scale-up phase.

Although the traditional EU approach is tilted toward preparing several frameworks, rolling out new regulations and targets, making funds available via dedicated units such as the European Investment Bank (EIB), it lacks a clear pathway for companies towards achieving the EU’s ambitious goals. For example, if we compare EU’s policy approach with that of the US and focus on the latter’s execution via the roll out of the Inflation Reduction Act (IRA), it can be concluded that the US IRA addressed multiple aspects of boosting demand creation as well as advancing local manufacturing by providing tax credits for domestic production and incentives for sourcing critical materials, in addition to clearly defining the eligibility requirements for companies to qualify for those tax credits.

The result was encouraging for the US. The IRA fetched billions of dollars in fresh investments into the country to strengthen the domestic supply chain while continuing to offload foreign dependency every subsequent year.

It is also noteworthy to mention that in a few instances, European policies have been self-contradictory, often making it difficult for companies to take clear decisions. For example, EU’s move to impose countervailing duties on the import of made-in-China BEVs only encouraged Chinese carmakers to ship hybrid vehicles, which attracted no additional import duty. With demand slowdown for BEVs and an increasing uptake of hybrid vehicles, it remains questionable how EU’s policy in this regard is not self-defeating.

Similarly, while the EU aims to bolster local manufacturing of batteries, it imposes almost negligible import duty of as low as 1.3% on the import of battery cells into the region. Moreover, reports suggest there is zero tariff on the import of sodium-ion batteries into the EU region. In comparison, the US has raised the import duty on lithium-ion battery cells imported from mainland China to 25%, from the previous rate of 7.5%, under the Biden administration. This was further raised to 58% on lithium-ion batteries imported from Greater China under the Trump administration.

标普全球移动出行展望

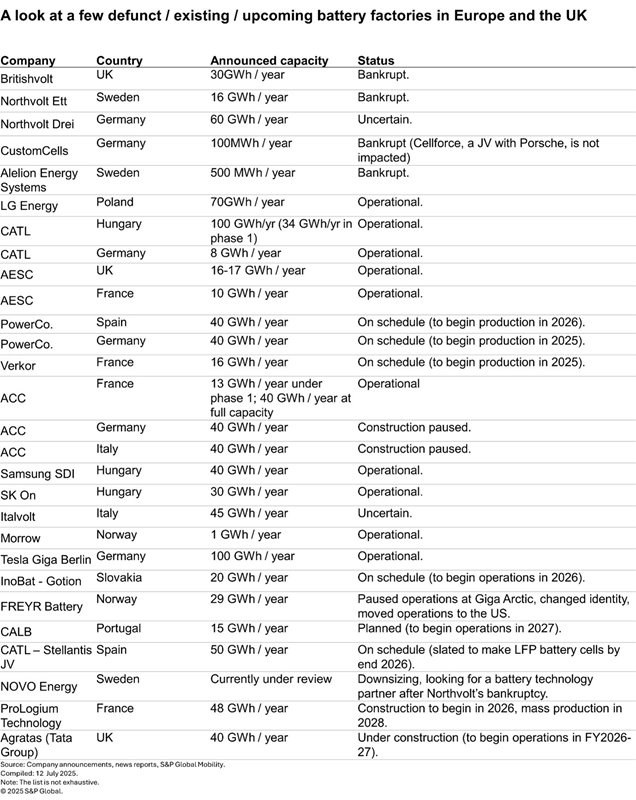

尽管存在这些结构性风险,过去两年间欧盟和英国仍宣布了多个新的电池制造项目。其中包括Agratas计划在英国萨默塞特郡建设的40GWh超级工厂。该超级工厂项目隶属于总部位于印度的塔塔集团,虽然施工工作已启动,但该工厂预计将在2026-27财年正式投产。

在政策层面,欧盟似乎正逐渐认识到需要对当地新兴电池企业提供更积极的支持。近期,欧盟委员会于7月4日宣布向该地区六个电池电芯制造项目提供总额8.52亿欧元的拨款,这一举措令人鼓舞。 这些项目包括ACC和Verkor在法国的超级工厂项目、Cellforce和Leclanche在德国的电池项目、沃尔沃支持的Novo Energy在瑞典的超级工厂,以及LG Energy Solution在波兰的电池工厂。

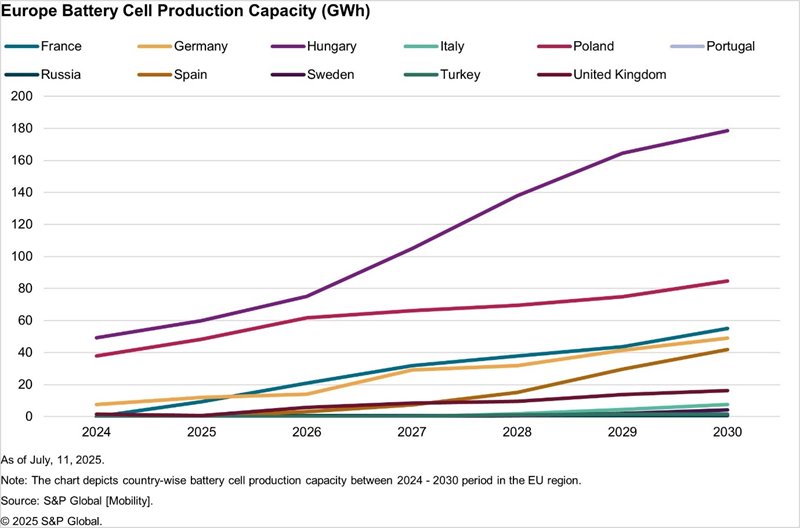

据标普全球移动(S&P Global Mobility)的数据预测,到2030年,匈牙利仍将是欧洲电池电芯产能排名第一的国家,随后依次是波兰、法国和德国。 匈牙利在欧盟电池电芯产能方面的领先地位,主要得益于其地理位置居中,更接近亚洲和中东地区。此外,该国不仅拥有整个欧盟地区最低的电价,与欧盟西部国家相比,还具备低成本劳动力资源。

标普全球移动出行(S&P Global Mobility)旗下电池研究部门(Battery Research)的阿迪姆(Adim)就欧盟地区现有及即将投产的超级工厂发表了看法,他表示:“欧洲电池生产的本土化主要出于自愿,同时也受到整车制造商为降低供应链风险而施加的压力。这意味着欧洲整车制造商愿意支付溢价来采购欧洲产电池,以降低地缘政治、运输和供应链风险。”

“目前,由于缺乏原产地规则且进口关税极低,欧洲电池制造商面临着廉价中国电芯的冲击。欧洲可能会采取保护主义措施予以应对,例如提供本地采购激励或提高进口电池电芯的关税。”

他还指出,磷酸铁锂(LFP)电池电芯产能不足仍是欧洲面临的主要挑战。 “ACC和PowerCo正根据客户对更廉价电池电芯的需求,重新审视其镍基战略,但大多数LFP电芯仍来自大中华区。尽管宁德时代(CATL)等中国供应商计划启动本地化生产,但对中企的依赖很可能持续甚至加剧。”

阿米特·潘戴

标普全球移动业务高级研究分析师

如需了解更多信息,请 点击此处