Lead times stretching beyond 24 months are reshaping the transformer value chain, creating both supply chain pressure and strategic growth opportunities for component suppliers.

Introduction: A Global Transformer Supply-Demand Imbalance

The global transformer industry is facing one of the most severe supply bottlenecks in decades. Lead times for large power transformers, which typically ran between 7 and 14 months before the pandemic, have stretched well beyond 24 months in most major markets. For some specialized units, procurement timelines are approaching 36 to 48 months. The International Energy Agency's (IEA) 2025 report "Building the Future Transmission Grid," based on a 2024 survey of industry participants, indicates that lead times have almost doubled on average since 2021, with manufacturers reporting record backlogs.

Demand for transformers, both distribution and power, is surging across key regional markets. PTR market intelligence indicates a significant rise in transformer demand across key regions such as Asia-Pacific (APAC), Europe, and North America by 2030. The drivers are structural: grid expansion and modernization, renewable energy integration, electrification of transport and industry, data center growth, and aging infrastructure replacement.

Yet manufacturing capacity has failed to keep pace. Transformer original equipment manufacturers (OEMs) are struggling to fulfill orders, resulting in longer lead times, extended production cycles, and growing bottlenecks in the supply of critical components. This strain extends well beyond the OEMs themselves. Component suppliers throughout the value chain are feeling the pressure too, as constrained transformer output reshapes procurement priorities and investment decisions. For those positioned to respond, the market presents meaningful strategic opportunities.

Power Transformers: The Segment Under the Greatest Pressure

Understanding Transformer Segments

Not all transformers face equal pressure. Distribution transformers are smaller, higher-volume units serving local networks. Their lead times peaked above 100 weeks in 2023 but have since eased. Power transformers are a different matter. These large, custom-engineered units operate at high-voltage levels in transmission networks and at generation step-up points. Each must be built to specific project requirements, individually tested and certified. They cannot be mass produced.

Why Power Transformers Are Facing the Longest Lead Times

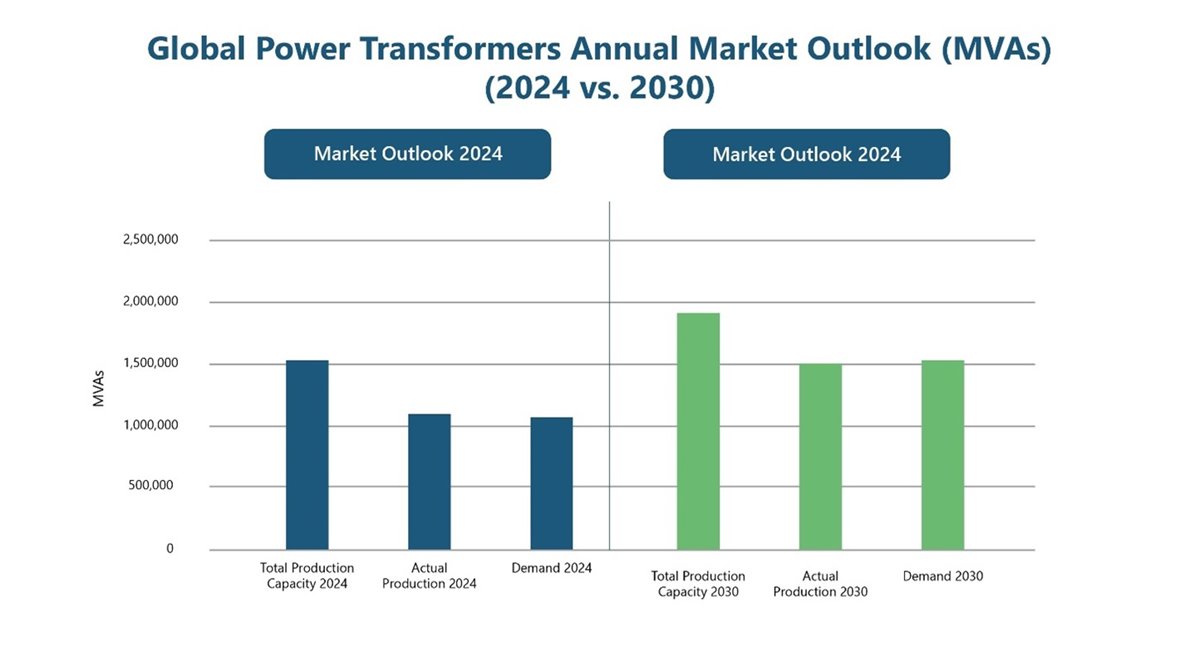

Large power transformers (LPTs) have seen the sharpest lead time increase of any segment. Before the pandemic, a typical LPT could be sourced in 12 to 14 months. Today, lead times in North America and Europe extend up to 60 months in some cases, compared to roughly 12 months in APAC. Four structural factors explain this: highly customized engineering, long manufacturing and testing cycles, dependence on a small set of specialized components, and a limited global base of manufacturers capable of producing the largest units. OEM utilization rates for LPT facilities currently average around 70% globally and are projected to reach 80% by 2030, leaving little room to absorb new demand spikes. Transformer prices have followed the same trajectory: the IEA's 2025 report found that in some cases prices have reached 2.6 times their pre-pandemic levels in real terms.

Picture available here, page 13.

Regional Trends in Transformer Lead Times

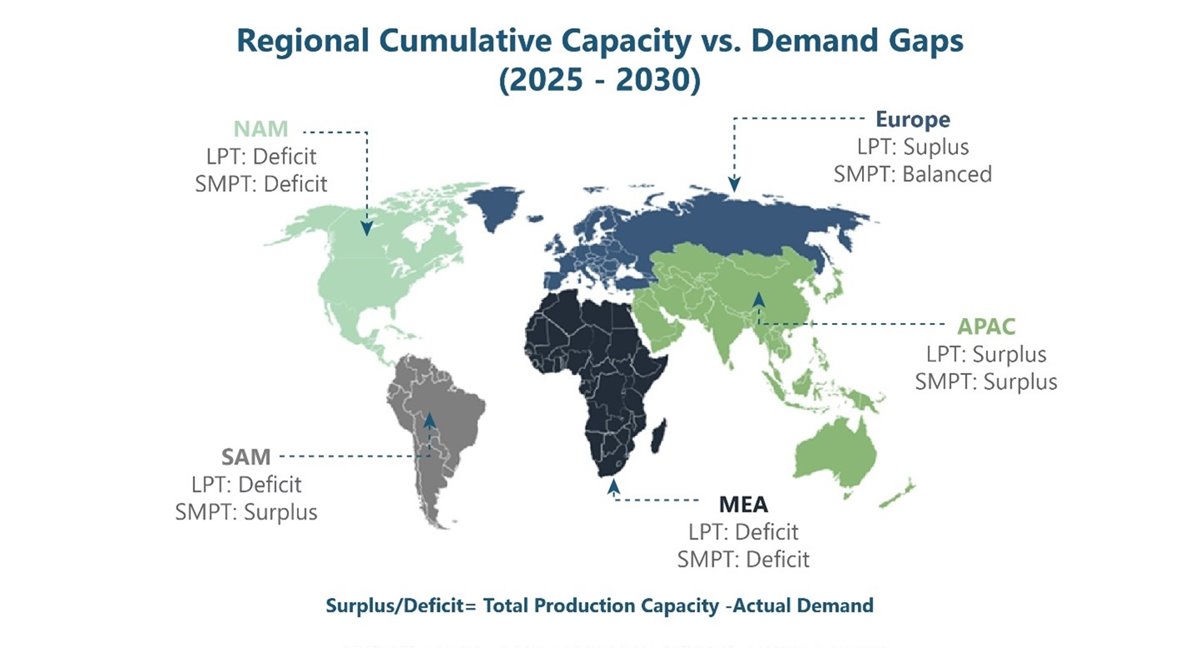

North America faces some of the most acute supply pressure globally. Over 70% of the US power grid is older than 25 years, and approximately 2.1% of the total transformer fleet is retired annually. Grid interconnection queues, renewable integration targets, and data center buildouts have all surged simultaneously. The US also relies on a single domestic producer of grain-oriented electrical steel (GOES), the core raw material in transformer manufacturing, making the supply chain particularly fragile. PTR projects a revenue compound annual growth rate (CAGR) of approximately 5% for the North American power transformer market from 2023 to 2030, with the US driving nearly 80% of regional demand.

Europe has a well-established manufacturing base and is a net exporter of LPTs, supplying approximately 40% of US LPT imports. However, rising internal demand is absorbing that capacity. The European power transformer market is projected to grow at a CAGR of 12.7% from 2024 to 2030, driven by high-voltage grid expansion, aging infrastructure replacement, and industrial electrification. The EU's target of 45% renewable energy by 2030 requires deployment of around 600 GW of solar and 510 GW of wind capacity, directly fueling transformer demand. LPT lead times in Europe currently range from 48 to 60 months.

APAC remains the world's largest manufacturing hub with the shortest lead times, averaging around 12 months for LPTs. However, strong domestic demand from China and India limits the capacity available to buyers elsewhere. PTR data identifies LPT and small-to-medium power transformer (SMPT) deficits in the Middle East and Africa through 2030, reflecting rapid grid expansion in those regions combined with near-total dependence on imports.

Picture available here, page 21.

The Component Supply Chain Behind Transformer Lead Times

A transformer build moves only as fast as its slowest component. GOES is the foundation of every transformer core and one of the most constrained inputs in the chain. US market data points to price increases of 60 to 70% since 2020, with Cleveland-Cliffs the sole domestic GOES producer. Copper is the other primary material input: the National Renewable Energy Laboratory's (NREL) 2024 study attributed current shortages in part to simultaneous pressure across GOES, copper, and aluminum, with copper prices rising nearly 10% in 2023 alone.

Beyond raw materials, high-voltage bushings and on-load tap changers (OLTCs) are the components most consistently flagged as build-schedule bottlenecks. Both are highly specialized, certified per application, and served by a limited number of qualified global suppliers. A delay in either holds up the entire transformer build regardless of how far along everything else is. Transformer oil and insulating fluids add further strain, as tightening sustainability requirements push manufacturers toward alternative fluid specifications that are not yet widely available.

Join global transformer manufacturers, component suppliers, and industry experts at CWIEME Berlin to explore solutions, build partnerships, and stay competitive in a rapidly evolving market.

Register nowImplications for Transformer Component Suppliers

From Vendors to Strategic Supply Partners

Component suppliers have traditionally competed on price and specification compliance. That dynamic is shifting. OEMs under pressure to shorten build timelines are pulling suppliers into procurement conversations much earlier. Long-term supply agreements are becoming standard practice. Supply reliability is now weighted alongside cost in qualification decisions, and OEMs are broadening their approved supplier bases to reduce single-source exposure, particularly for GOES, bushings, and OLTCs.

Growing Opportunities in Key Component Segments

Bushing manufacturers benefit directly from sustained high-voltage transmission buildouts across all major regions. OLTC suppliers operate in a concentrated market where any disruption has outsized downstream consequences. GOES and core material producers face a capacity investment challenge: new production lines take years to commission and require long-term demand visibility to justify. The nearly USD 1.8 billion in OEM manufacturing investments announced across North America alone since 2023 represent real downstream demand for regionally positioned component suppliers.

Localization and Supply Chain Diversification

Geographic proximity is becoming a genuine competitive differentiator. Both utilities and OEMs are under growing pressure to demonstrate supply chain resilience. For component makers, the ability to supply OEM manufacturing clusters in North America and Europe is now a meaningful advantage in supplier qualification, not just a logistical convenience.

Conclusion: A Structural Shift in the Transformer Supply Chain

Lead times of 24 months and beyond are not temporary disruptions. NREL projects that US distribution transformer capacity may need to grow by 160 to 260% by 2050 relative to 2021 levels. PTR market intelligence points to sustained growth through 2030 across all principal markets, with demand reinforced simultaneously by grid modernization, renewable integration, industrial electrification, and data center expansion.

In this environment, component suppliers have moved from the background of the transformer value chain to a position of genuine strategic importance. Those who invest in capacity, build closer OEM relationships, and demonstrate consistent supply reliability are well placed to grow with a market that is expanding for structural, not cyclical, reasons. The opportunity for component suppliers to define their role in this shift is open now.

About the Author:

.jpg)

Azhar Fayyaz

Senior Analyst II- PTR

Azhar Fayyaz is a Senior Analyst II and leads transformer research at PTR.Inc, supporting global clients with insights on transformers, switchgear, and substation automation. With a technical background and an MSc in Power Engineering, he offers deep domain expertise and practical analysis.

About PTR:

With over a decade of experience in the Power Grid and New Energy sectors, PTR Inc. has evolved from a core market research firm into a comprehensive Strategic Growth Partner, empowering clients’ transitions and growth in the renewable energy landscape and E-mobility, particularly within the electrical infrastructure manufacturing space.

Contact:

([email protected])